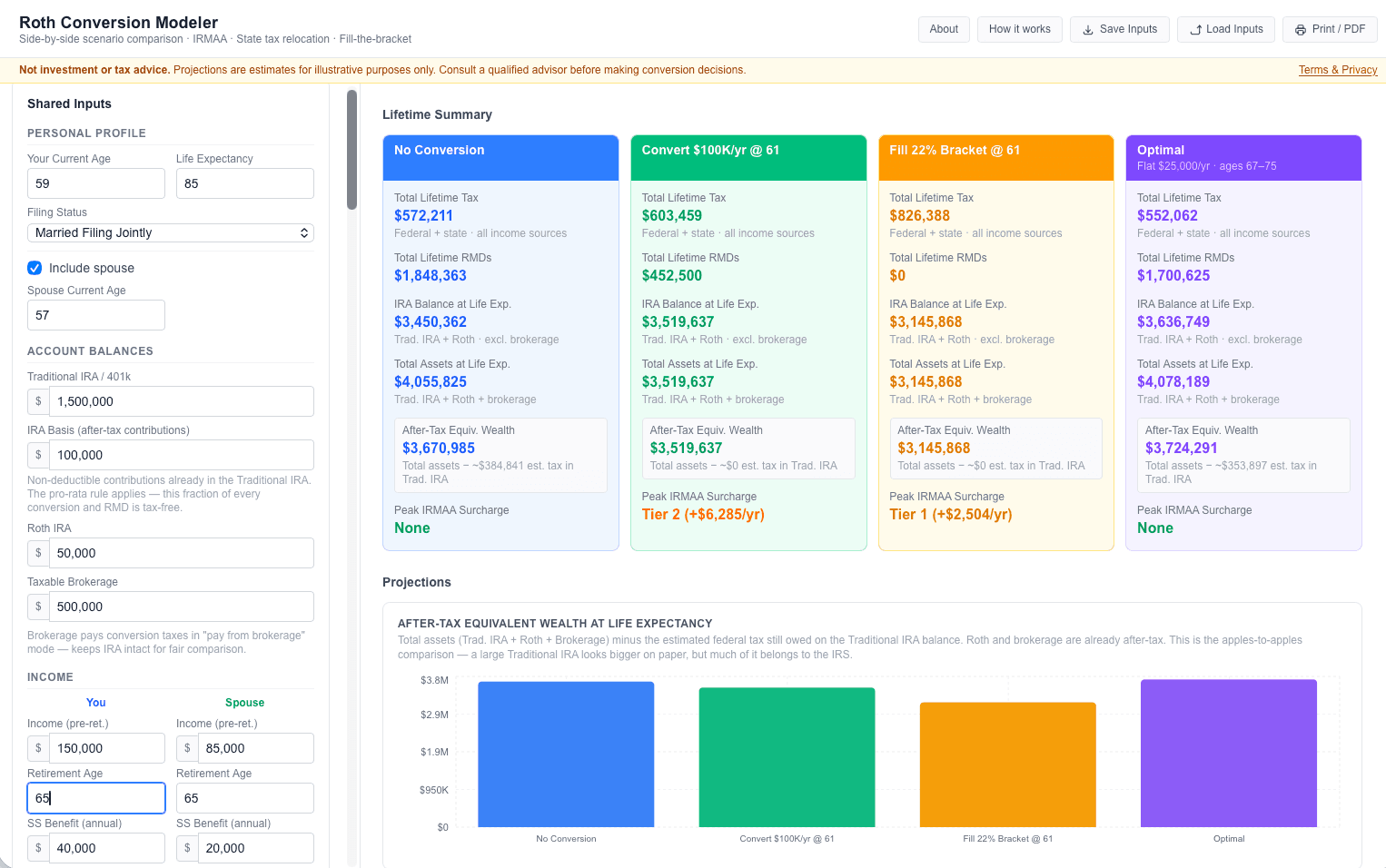

Model your Roth conversions side‑by‑side.

Build up to three conversion strategies, then let the optimizer search dozens more and surface the one that maximizes your after-tax wealth — with IRMAA, Social Security taxation, and RMDs all modeled.

Open the modeler →

From situation to strategy in three steps.

Enter your situation

Ages, balances, ordinary income, Social Security claiming, pension, expenses. Both spouses if you have one.

Build three scenarios

No conversion, flat $/yr, or fill-the-bracket. Different ages, different states, different tax-payment sources.

Consider the AI optimal scenario

Charts and tables update live. The AI Optimal scenario shows what the search algorithm found.

The interactions that wreck a flat-rate comparison.

Most calculators ask for a “current rate” and a “future rate” and call it a day. Roth conversions are nonlinear and they compound for decades. Here’s what we model that they don’t.

SS taxation thresholds

A conversion can push 50% — then 85% — of your benefit into taxable territory. Stacked the way the IRS does.

IRMAA two-year lookback

Year-by-year MAGI tracked against inflated tier thresholds. See exactly when you cross.

Couples, properly

Separate income, retirement, and SS claiming per spouse. Both timelines tracked independently.

After-tax equivalent wealth

Embedded tax liability on traditional balances deducted before comparing. The honest number.

Three custom scenarios

Different amounts, ages, brackets, states, tax-payment sources. All update live.

AI optimal search

Grid-searches dozens of strategies and surfaces the after-tax winner — and tells you why.

You shouldn’t have to guess at the right strategy.

The optimizer searches across bracket fills, flat amounts, start ages, and end ages — then explains the winner by comparing today’s marginal conversion rate against tomorrow’s RMD rate.

Run it alongside your own three scenarios. If you can beat it, you understand your situation better than the algorithm — and that’s worth knowing too.

Ready when you are.

~3 minutes to enter your situation. Save a session and come back to it later.